/ICX_Insights%20content/Folder%20icon%20for%20insights.svg)

/ICX_Insights%20content/Folder%20celeste.svg)

/ICX_Insights%20content/Print%20gris.svg)

/ICX_Insights%20content/Print%20celeste.svg)

/ICX_Insights%20content/Share%20icon.svg)

/ICX_Insights%20content/Share%20celeste.svg)

/ICX_Insights%20content/Subscribe%20icon.svg)

/ICX_Insights%20content/Subscribe%20celeste.svg)

/ICX_Insights%20content/Start%20Here%20icon.svg)

/ICX_Insights%20content/Start%20here%20celeste.svg)

Stop chasing costs—Your biggest profit lever is pricing

There is an idea that is repeated in many budget meetings: "First let's fix the costs; then we see the price." I myself was a staunch defender of...

8 min read

8 min read

In many meetings with CEOs, CFOs and commercial managers we hear the same phrase, almost copied, even if the country or industry changes:

"We are selling more than ever... but the usefulness does not appear."

From there, a familiar script opens: finance arrives with worrying numbers, sales defends that "without discounts it does not close", operations feels the pressure to produce more with the same budget and the general manager ends up acting as an arbitrator between areas that, in theory, should be aligned towards the same objective.

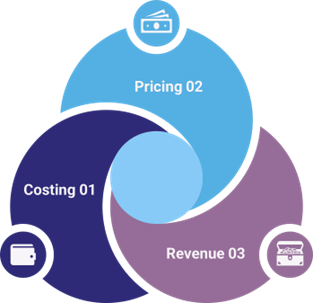

At ICX we saw that pattern so many times that we decided to do more than just "put out fires" on a case-by-case basis. This is where the PCR methodology was born : Pricing, Costing and Revenue. Not as a nice name for a presentation, but rather as a working system that connects three dimensions that are almost always managed separately: how costs are calculated, how prices and discounts are defined, and how the business process is executed on a day-to-day basis.

>> What is pricing and how does it differ from Revenue Management? <<

When we first enter an organization, we almost never encounter total chaos. What we usually find is a partial order. Finance has its statements up to date. Comercial has sales reports, quotas and forecasts. Operations knows exactly how many shifts it needs to meet demand. But when we start asking uncomfortable questions, (which is what we consultants do) the sense of control cracks.

We ask, for example:

And there are silences, estimates "by the eye of a good cubero" as it is popularly said. Excel sheets that someone updates when they can and costing models that serve for accounting purposes and more or less to make a quote, but not to make fine business decisions.

In practice, many businesses live with a dangerous paradox: they can show growth in sales, but without the ability to explain why profit does not grow in the same way. That gap is what we attack with PCR.

PCR starts from a very simple conviction:

You can't seriously talk about prices if there is no clarity about costs, you can't talk about revenue if the commercial process is not aligned with profitability, and you can't talk about sustainable profitability if these three elements are governed as islands.

In most companies, costing, pricing and revenue management are managed in different lanes.

In costing, it is common to find:

In pricing, we see:

And in revenue, the focus is almost always on:

When we look at these three pieces separately, it seems that the system works. But when we connect them, contradictions appear: products that sell a lot but destroy value, large customers with conditions that no one dares to review, commissions that pay by volume even when the margin evaporates.

The PCR methodology brings these conversations together into a single framework. Instead of talking about costing "on one side", prices "on the other" and sales "over there", we began to see the business as a system where every price decision and every commercial policy is based on the real cost and a clear vision of profitability.

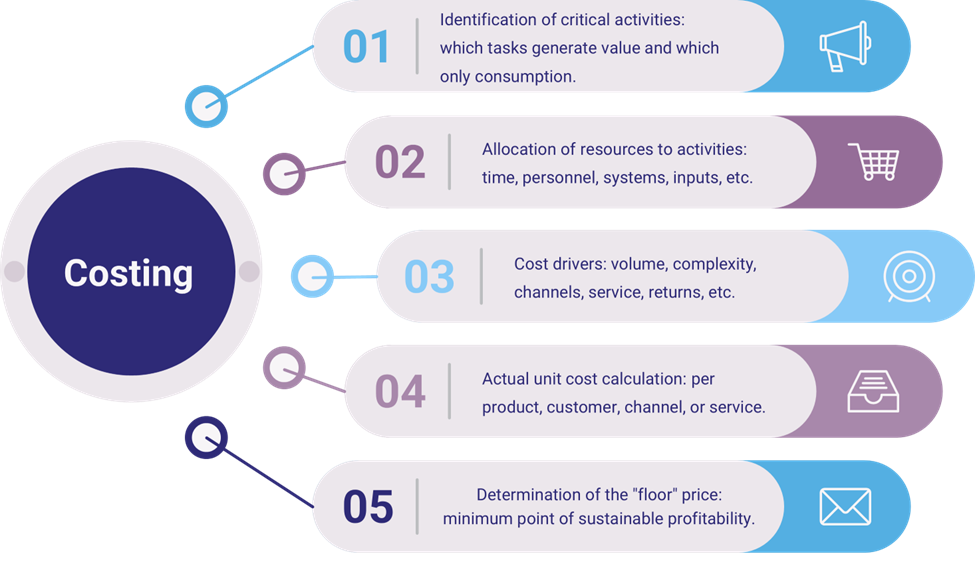

The first major pillar of PCR is actual costing. I'm not just talking about knowing how much it cost to produce in general, but also about understanding the real unit cost per SKU, considering both direct and indirect costs with consumption drivers.

When we ask a company for the unit cost of a specific product, it's not uncommon to hear answers like:

"We have it by family, not by SKU." - "We calculate it once a year to adjust prices." - "We can approximate it, but not very precisely." - "We have it but only with the direct and indirect costs of manufacturing, but they are the administrative overhead" (the latter is the classic).

These cases are understandable, but they are also risky. Making pricing and portfolio decisions on that basis is like piloting an airplane with an altimeter that works "more or less."

At PCR, what we do is reconstruct that instrumentation. We review how direct costs (raw materials, direct labor, packaging) and indirect costs (energy, maintenance, logistics, commercial administration, etc.) are being allocated today. Then, we define consumption drivers that allow indirect costs to be allocated more fairly and closer to the operational reality: machine hours, number of setups, order lines, kilometers traveled, deliveries made, among others.

This change, which on paper seems technical, has very concrete effects: we suddenly discover that certain "star" SKUs in volume are actually silent destroyers of value. These are products that require more line changes, more logistical handling, more expensive packaging per unit and very frequent small orders. When those costs are allocated accordingly, the notional margin becomes negative margin.

Imagine, for example, a portfolio of cleaning products with three presentations of the same detergent: small, medium and large. Without a model with drivers, it may seem that the three share a fairly similar return. With a PCR model, another truth often emerges: the small presentation is much more expensive to manage than the averages reflect. Selling it "because it rotates faster" can end up being a bad deal if price, packaging or process is not adjusted.

It is not a question of doing more complex accounting for sport. It's about having a firm, defensible floor for everything that comes after: pricing, discounts, portfolio decisions, negotiations with key clients, and commission design.

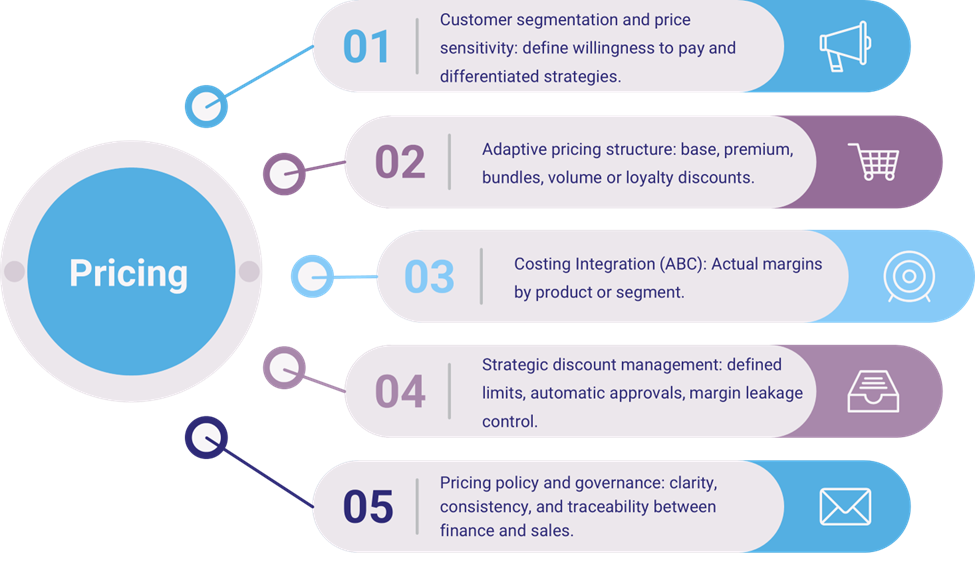

Once there is clarity about the true cost, the price conversation changes its tone completely.

We can say that the price is a mixture of history, custom and commercial urgencies. There are lists that have been adjusted for inflation, discount policies that grew by exception until they became the norm and a generalized logic of "we'll see the margin in the end". The result is an environment where every important account is negotiated almost from scratch, and where the salesperson is halfway between taking care of the customer relationship and protecting the margin of the business.

At PCR, we talk about designing a pricing and discount architecture, not about "throwing away a percentage increase". This architecture starts from the real cost as a floor and builds around a possible price range according to segment, channel, region, type of customer, perceived value and role of each product in the portfolio.

Instead of seeing discounts as chaotic concessions, we began to treat them as tools of explicit policy. When does it make sense to give a bigger discount? When the client assumes a volume commitment, when the payment term is improved, when there is exclusivity, when there is a long-term contract. All of this can become the rule, instead of remaining the "personal judgment of each salesperson".

Let's go back to the case of the small presentation of value-destroying detergent. With PCR on the table, we can define certain rules to play with, such as:

In this way, the price ceases to be an isolated number and becomes a decision consistent with the profitability strategy.

The third pillar of PCR looks at the business process head-on. It is not enough to have clear costs and well-designed prices if the day-to-day sales respond to another logic.

In many companies, the commercial area is still measured almost exclusively by volume: how much was sold, how much was invoiced, what percentage of the quota was met. The problem is that, with these indicators, the sale of unprofitable products, excessive discounts and negotiations that "save the month" but compromise the accumulated margin of the year are also rewarded.

With PCR we review the sales funnel and the systems that support it, usually in the CRM. We don't just map stages; We analyze how the tool is actually being used: what is registered, what is omitted, where opportunities are lost, where reprocesses are multiplying. The goal is to turn CRM into an ally to manage profitability, not just use it as "an expensive Excel" as we call it.

This implies, among other things, introducing into the commercial conversation variables that are traditionally only talked about in finance: mix of profitable and unprofitable products per customer, impact of discounts on the margin, different behaviors by channel, concentration of the portfolio in value-destroying products, etc.

From there, we began to redesign indicators and incentives. The question is no longer just "how much did each salesperson sell?", but "what quality of mix did they sell?", "how much margin did they contribute?", "what percentage of their sales came from strategic lines?". Commissions may still be simple to manage, but they are no longer indifferent to the product being sold.

Consider a sales team that charges a fixed commission on gross sales. Under this scheme, the most logical way to maximize personal income is to push the products that the customer accepts faster, not necessarily the most profitable ones. With PCR, that logic is corrected: products with a high contribution to profit may have more attractive commissions, while products that are "drawn" or with negative profit require different treatment. That doesn't just protect the margin; It also directs sales energy to where the company actually wins.

One of the most tense moments of a PCR project is when we put the portfolio profitability analysis on the table. There are always products that surprise: those that the market "loves", that Comercial defends tooth and nail, but that, in terms of result, consume more than they contribute.

The impulsive reaction may be: "they must be eliminated". But in practice it is not that simple. Some of these products maintain a brand image, complete a necessary offer for certain customers or take advantage of installed capacity that, without them, would be idle. Other times, they are the gateway to relationships that then become highly profitable with other products and services. In PCR we do not arrive with the axe in our hands. We arrive with a question: if this product destroys value in the current conditions, what options do we have to stop it?

The answers usually go through several layers: reviewing specifications and raw materials, renegotiating with suppliers, adjusting packaging to reduce handling costs, rethinking production batches, redefining presentations, changing channel strategy, repositioning the product towards segments that are willing to pay more, creating packages or subscriptions where the product alone may not be a business, but as part of an integrated offer, yes.

Only when these alternatives have been explored and the numbers are still in the red does elimination become a serious option. And when that happens, the conversation with general management is based on clear scenarios: what happens if the product is left as is, what happens if it is redesigned, what happens if it is eliminated and how that space in the portfolio is compensated.

A very reasonable question we are asked at the beginning is how long all this takes and what it implies for the internal team.

Experience has led us to work PCR in three major moments.

The first is the diagnosis, which we concentrate in about a month. It is not a superficial diagnosis, but neither is it an endless study. During that time, we analyzed how costs are being calculated today, how many layers of detail there are, how prices and discounts are structured, what real use CRM has and how commercial performance is measured. At the closing, we present a clear map of gaps and opportunities, along with impact hypotheses: where we suspect value destruction is occurring, where products or customers are being subsidized, and what decisions could generate visible improvements in the short term.

The second moment is execution, which usually lasts between six and nine months. There we built the costing model with consumption drivers, defined the pricing architecture and discount policies, reconfigured the CRM to incorporate profitability logics, redesigned indicators and incentives and accompanied the first portfolio and pricing decisions. It is an intense phase, but very practical, here we work together with people from finance, commercial and operations, together and not in isolation.

The third moment is accompaniment, which can reach up to twenty-four months. Why so much? Because reality changes: costs go up and down, the product mix evolves, new competitors appear, market conditions change. Without structured follow-up, it is very easy for the organization to return to its old habits: discounts for pressure of the month, business decisions that do not consider the cost model, indicators that return to what is known. At this stage, our role is to help keep the PCR system alive, adjust when necessary, and continue to generate insights from the data.

PCR is not a project that is "delivered" and archived. It is a change in the way of thinking and talking about the business.

There is an idea that is repeated in many budget meetings: "First let's fix the costs; then we see the price." I myself was a staunch defender of...

Imagine running a company without really knowing how much it costs to produce what you're selling. How could you set competitive prices, identify...

If you’ve read my article titled “Top Tips for Making Your Cost Model a Total Disaster”, you’ll know that one of the factors that can kill a cost...